Check out the biggest breaking crypto market updates for today:

Tokenized FTX Claim Is Used As Collateral For A Loan

According to the bankruptcy claims platform Found, an FTX creditor has made history by making the first on-chain loan backed by an FTX claim. The creditor reportedly pledged his claim as collateral for a loan in the DeFi protocol Arcade.

The claim which is worth $31,307 was tokenized and used as collateral for a $7,500 loan to be repaid in five days.

The transaction is an example of a real-world assets (RWA) tokenization, in which a token represents an asset’s ownership rights on a blockchain. Within DeFi, asset tokenization is one of the most prominent areas, as a wide range of real-world assets can be tokenized, including stocks, government bonds, real estate and commodities.

On Twitter, Found said the original creditor and lender went through its biometric Know Your Customer and Anti-Money Laundering screenings. According to the company’s website, it allows users to access loans using bankruptcy claims as collaterals under a 10% transaction fee on successful trades.

Crypto exchange FTX filed for bankruptcy in November 2022, locking billions of dollars in users’ accounts for court proceedings. According to some estimates, FTX claim holders could recover between 35% and 66% of their face value.

Crypto-related bankruptcy cases have flooded the courts in the past year – many stemming from the collapse of FTX – including cases associated with crypto firms Genesis Global Trading and BlockFi.

The surge in bankruptcy filings is driving on-chain claims solutions. Found, for example, was launched at the beginning of this year, and the co-founders of collapsed hedge fund Three Arrows Capital launched the claims trading platform Open Exchange in April.

Robinhood Lays Off About 7% Of Its Full-Time Employees

According to a Wall Street Journal report, crypto and equities brokerage firm Robinhood has laid off about 150 employees (roughly 7% of its staff) in order to “adjust to volumes and to better align team structures.”

Notably, this is the firm’s third round of layoffs in just over a year.

A Robinhood spokesperson stated,

“We’re ensuring operational excellence in how we work together on an ongoing basis. In some cases, this may mean teams make changes based on volume, workload, org design, and more.”

The company previously cut more than 1,000 jobs in two rounds of layoffs in 2022. The restructuring affected roles in customer experience, platform shared services, customer trust and safety, and safety and productivity.

The company experienced an uptick in employees voluntarily leaving and declines in reported employee job satisfaction following the layoffs in 2022.

The layoffs come shortly after Robinhood announced its agreement to acquire credit-card startup X1 in a $95 million cash deal, indicating the company’s move to expand its product offerings beyond trading.

Robinhood had a significant rise in popularity during the pandemic, attracting millions of users for stock, options, and cryptocurrency trading.

But by May 2023, the company reported fewer than 11 million monthly active users, and its transaction-based revenue dropped 5% year-over-year in Q1 2023.

Despite the layoffs, Robinhood’s shares are up about 18% this year, but still down about 86% from a record high shortly after the company’s public debut in 2021.

FTX Has Recovered $7B In Assets So Far, Has Almost $2B To Go To Cover Misappropriations

According to a second investigative report released by FTX debtors on Monday, FTX has recovered about $7 billion in liquid assets, with the search for additional assets still continuing.

The report currently estimates the amount of customer assets misappropriated by FTX at $8.7 billion, with $6.4 billion of it held in the form of fiat and stablecoins, which FTX did not differentiate between in its accounting.

CEO and Chief Restructuring Officer John J. Ray III stated,

“The image that the FTX Group sought to portray as the customer-focused leader of the digital age was a mirage. From the inception of the FTX.com exchange, the FTX Group commingled customer deposits and corporate funds, and misused them with abandon at the direction and by the design of previous senior executives.”

The report alleged the former FTX leadership “did not commingle and misuse customer deposits by accident,” and leadership hid its actions “with the assistance of a senior FTX Group attorney” and others.

As a result,

“Notwithstanding extensive work by experts in forensic accounting, asset tracing and recovery, and blockchain analytics, among other areas, it is extremely challenging to trace substantial assets of the Debtors to any particular source of funding, or to differentiate between the FTX Group’s operating funds and deposits made by its customers.”

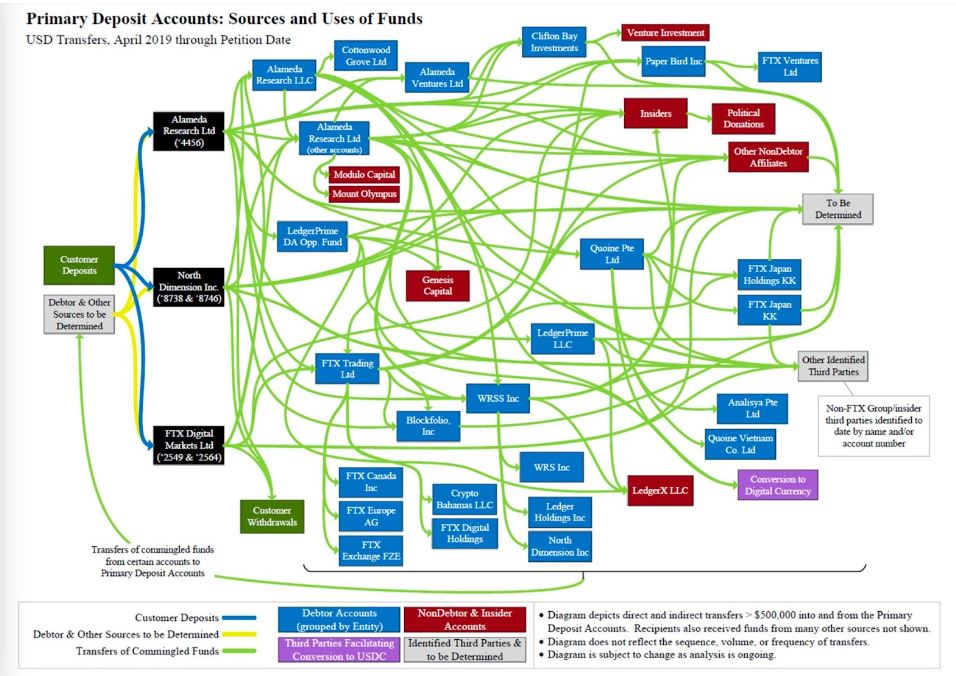

The extent of the chaos was driven home by a diagram of flows of FTXcustomer money out of primary deposit accounts “as identified to date.” Those flows were made possible by misrepresenting their purpose to banks and many other false representations, the report said.

Here’s the flowchart of where funds were going at FTX prior to its collapse:

The misrepresentation even extended to statements former CEO Sam Bankman-Fried (SBF) made to the United States Congress. The involvement of the unidentified FTX senior attorney was mentioned repeatedly, and it was noted that the attorney fired a less senior attorney who raised objections to the company’s deceptive practices.

Misappropriated funds were used for political and charitable donations and the company’s investments and acquisitions, such as luxury real estate, the report alleged

“The FTX Senior Executives [SBF, Gary Wang and Nishad Singh] and [Alameda Research CEO Caroline] Ellison informally tracked the size of FTX.com’s undisclosed, fiat currency liability to customers that resulted from the extensive commingling and misuse of FTX.com customer deposits,” the report said.

Their estimates ranged from $8.9 billion to $10 billion, which is somewhat higher than the FTX Debtors’ estimate.

That is why I made my site - Stock Maven. Now that I feel settled and confident about trading, I want to be a source of help to anyone else who might be struggling to break into the crypto market successfully.

My website is full of my tips and tricks, as well as information that I have always found interesting about crypto. My friends and family are sick of hearing me talk about it, so now it’s your turn!

I hope that you stick around and find something useful on my site. Remember, to make it big in crypto, you’ve got to be confident! Go for it and don’t look back.

- Best AI ETFs for Beginners: Top 7 Picks to Start in 2026 - June 1, 2026

- Goal Based Crypto Investing: 2026 Long-Term Strategy Guide - May 30, 2026

- AI Penny Stocks With Potential: Top 10 Real Picks for 2026 - May 28, 2026